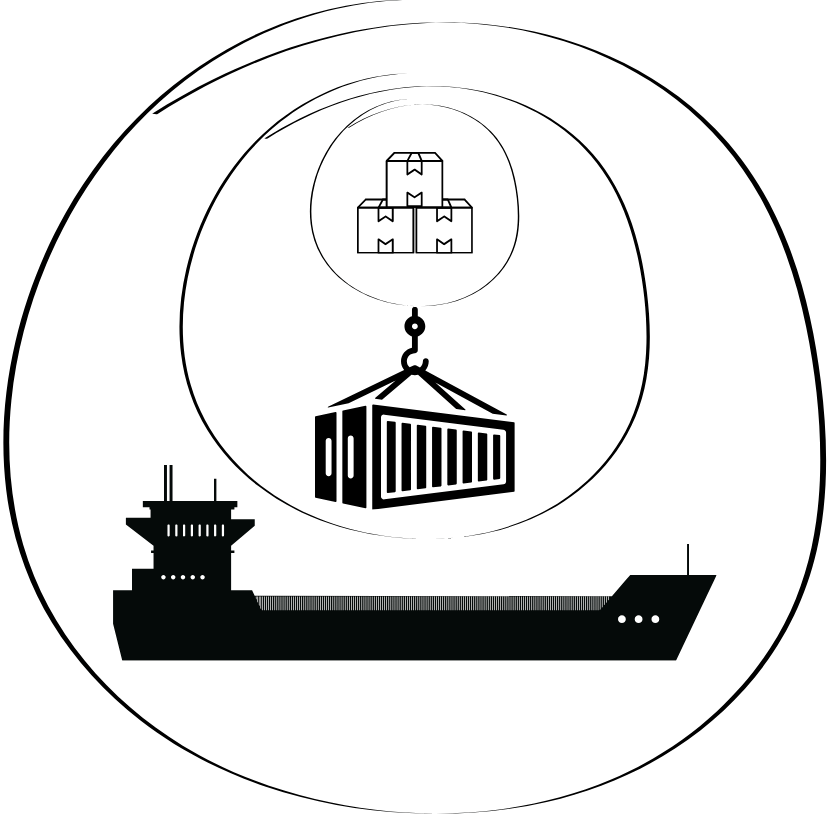

To invest, you need an account that holds and, in some cases, manages your capital, much like a cargo ship transporting containers (funds) which in turn contain hundreds of boxes or products (assets).

In the UK, the most common account types or ‘tax wrappers’ are offered through investment platforms, banks, insurance companies, or other investment firms. Here are some of the options:

Individual Savings Accounts (ISAs)

Stocks & Shares ISAs – These accounts allow investments in various assets and funds with no tax on gains and dividends, and no set limits on when you can access your money, providing both flexibility and tax efficiency. However, there is a limit to how much you can contribute each year.

Junior ISAs (JISAs) – Designed for children under 18, these accounts lock the funds until the child turns 18. Investments grow tax-free, making them a good option for long-term savings for minors. Again, there is a limit to how much you can contribute each year.

GIA (General Investment Account)

A GIA provides a flexible way to invest in various assets and funds with no annual contribution limits. Unlike ISAs, there are no specific tax advantages, and any gains are subject to capital gains tax.

Pensions

A pension is a way to save money for retirement. Both individuals and employers can contribute to these funds, which are locked until retirement, offering tax benefits to encourage saving for later life.

SIPP (Self-Invested Personal Pension) – A SIPP offers more control over retirement savings by allowing investments in a variety of assets, such as stocks and real estate, as well as funds. These investments can be managed by yourself. While offering tax reliefs, funds can’t be accessed until later in life, ensuring they are used for retirement.

Workplace Pensions – Set up by employers, these pensions involve contributions from both employer and employee, often with the employer matching contributions up to a certain level. Benefits from workplace pensions are accessible in later life and offer similar tax advantages to personal pensions.

Investment Bonds

Onshore Bonds – These are insurance-based investments with some life cover, offering tax-deferred growth and potential for tax-efficient withdrawals. Early withdrawals might come with surrender charges.

Offshore Bonds – Offering similar benefits to onshore bonds but based in low-tax jurisdictions, these allow for tax-efficient growth and withdrawals, also subject to surrender charges if accessed early.

These investment products and ‘tax wrappers’ can be defined by four factors:

Purpose – Although there are similarities, each product usually has a specific purpose.

Tax Benefits – These benefits don’t just happen by magic; they are designed by the government to encourage saving. These incentives come with a set of conditions that must be met.

Access Restrictions – Among these conditions are when and how you can retrieve your money. The incentives are not free. Just like when you received an allowance for tidying your room, the government offers incentives in exchange for being a “good saver.”

Regulation – The different types of accounts are regulated under their own legal framework that dictates how they must be managed, what information they must provide, and how the interests of investors are protected.

The most appropriate ‘wrappers’ or products will depend on your personal circumstances. When making a recommendation, your adviser should be able to answer the following questions:

What kind of assets does the product invest in? Fixed income, equities, alternatives, or a mix of these.

How does the product invest? Directly by purchasing financial assets on the market or through one (or several) investment funds?

Who manages the funds? Are they managed by the same entity selling you the product, or are they funds from other entities? Are they active or passive?

If the product contains a mix of funds, who selects these funds and who decides the percentage invested in each?

What are the tax benefits of the product? Why is this the best product for you compared to others?

Can you easily retrieve your money? If not, what are the advantages to compensate for this lack of access?

What are the costs of the product? Is it possible to distinguish between management fees and administrative costs?

The value of financial advice goes far beyond saying “buy here, sell there.” It’s about discovering your objectives and fears to help you find the solutions that best suit your needs. A good financial advisor should be a thinking partner who gives you confidence in major decisions and motivates you to pursue your goals.